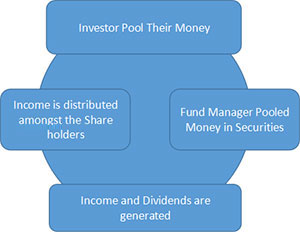

As the name suggests, a ‘Mutual Fund’ is an investment vehicle that allows several investors to pool their resources in order to purchase stocks, bonds and other securities.

These collective funds (referred to as Assets Under Management or AUM) are then invested by an expert fund manager appointed by a mutual fund company (called Asset Management Company or AMC).

The combined underlying holding of the fund is known as the

‘Portfolio’, and each investor owns a portion of this portfolio in form of units.

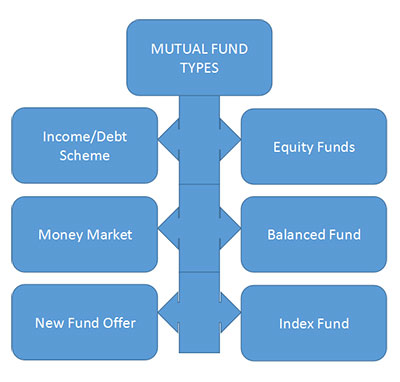

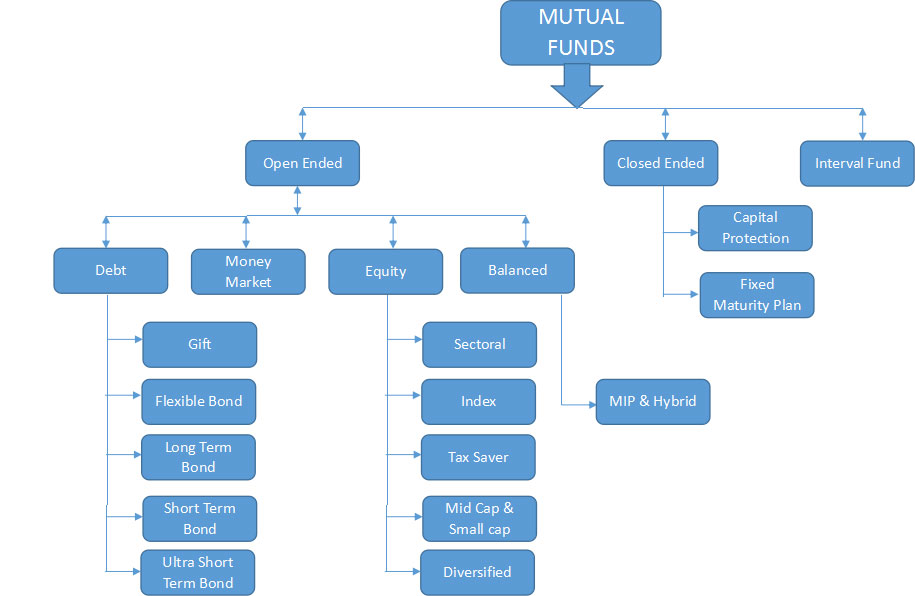

Considering to invest in Mutual Funds? It is important that you understand the types of mutual funds and their features. Mutual funds can be classified based on the following characteristics.

Based on Asset Class

Based on Structure

Based on Investment Goals

Based on Risk

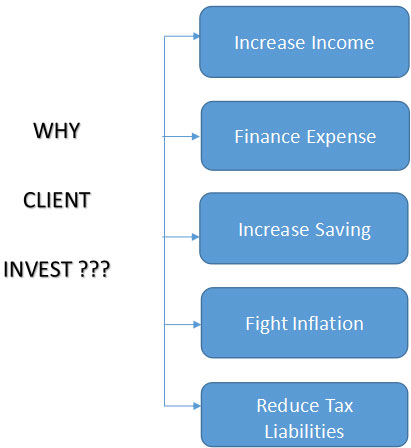

WHY CLIENT INVEST ???

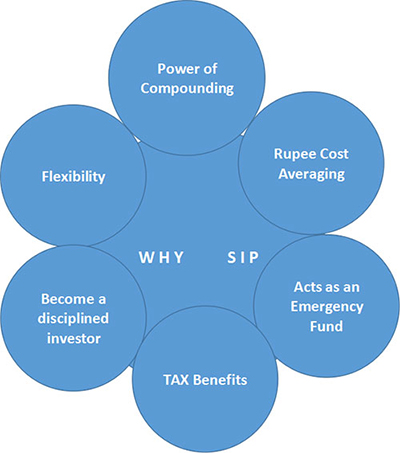

A Systematic Investment Plan (SIP) is an investment vehicle offered by mutual funds to investors, allowing them to invest small amounts periodically instead of lump sums. The frequency of investment is usually weekly, monthly or quarterly.

In SIPs, a fixed amount of money is debited by the investors in bank accounts periodically and invested in a specified mutual fund. The investor is allocated a number of units according to the current Net asset value. Every time a sum is invested, more units are added to the investors account.

The strategy claims to free the investors from speculating in volatile markets by Rupee Cost Averaging. As the investor is getting more units when the price is low and less units when the price is high, in the long run, the average cost per unit is supposed to be lower.

SIP claims to encourage disciplined investment. SIPs are flexible, the investors may stop investing a plan anytime or may choose to increase or decrease the investment amount. SIP is usually recommended to retail investors who do not have the resources to pursue active investment.

No need to time the markets

Imagine, if you could always pick the right time to buy and sell. However, timing the

market is a time-consuming and risky task. Through disciplined and regular investments,

you can stop worrying about when and how much to invest. In short, it eliminates the need

to actively track the markets.

Rupee cost averaging

Since your investments are spread regularly over a period of time, buying fewer units during

rising markets and buying more units during falling markets reduces the average cost per

unit of your investments - this concept is known as Rupee Cost Averaging.

Lowest Locking period

Compared to other tax-saving options, ELSS has the lowest lock-in period of 3 years.

Being an equity fund, it will be advisable to stay invested for a longer duration.

Best Tax saving investment under Sec 80C

It helps you to avail tax deduction under Section 80C in the EEE format i.e. tax exemption,

wealth accumulation and zero exit load.

Power of Compounding

Compound interest ensures better long-term benefits compared to one time investment

2x Higher returns than RD

As compared to the conventional FDs, ELSS gives higher returns to beat inflation in an efficient manner.

One-time investment

In this mode, you make a one time payment of a considerable sum of money.

Monthly SIP

On the other hand, in an SIP, a fixed amount of sum is deposited at regular intervals of time in

a mutual fund scheme. In short, one-time investment mode can be chosen if you have money

in hand right now that can be invested and an SIP can be chosen if you are expecting a regular

inflow of money in future.

| SIP Investment | One-time Investment |

| Periodic investments in a tenure | One-time investment in a tenure (lump sum) |

| Earns better during market lows | Earns better during market highs |

| SIPs can protect investments from potential market crash | One-time investments can lead to major loss during market crash, which happens often enough |

Our Most important mission is your Growth no matter, it’s our regular or direct client, we are always aware that in the end we are generating wealth for someone’s hard earned resources. We strive to deserve their trust in our character and competence through effective Management.

There are some things we just won't do for money. For example, Binduwasini’s does not recommend tobacco companies for its clients' portfolios. Here are our central tenets.

1. Track Record.

No matter the fancy tales money managers tell you, it all boils down to one number: the internal rate of return. Over the long term, this number, properly calculated and verified, will not lie.

2. Small Capital.

It's much easier to profitably invest smaller amounts of capital than larger ones, all other things being equal.

3. You Earn, We Earn.

We are sticklers for this one. We do not charge a single rupee in fees which is not linked to our performance. This distinguishes us from most of our peers.

A disciplined approach is vital.

Investing is neither a science nor an art -- it is a craft. Judgment calls must be made and risks must be taken. To be best positioned for the upside, it is important to have researched well.

Keep it simple, silly.

If there are a bunch of formulas and Greek letters involved, we stay away. Correlation coefficients and efficient frontiers are not for us, thank you.

BAJAJ FINSERV

RATED BY CRISIL - FAAA ( Highest Safety )

ICRA - MAAA ( Stable )

Need to Know

Credit ratings by agencies can help you make smarter investment choices in such cases. CRISIL is one such global analytical company that provides ratings, research, along with risk and policy advisory services. It is India’s first credit rating agency, which has pioneered the concept of credit rating in the nation.

Bajaj Finance Fixed Deposits have a FAAA/Stable rating from CRISIL, which indicates the highest safety and lowest investment risk.

Bajaj Finance FD’s also have a rating of MAAA (stable) from ICRA, which is another reason to invest in them.

MEANING OF CRISIL RATING

NM Not Meaningful

FD Default

FC High risk

FB Inadequate safety

FA Adequate Safety

FAA High Safety

FAAA Highest Safety

Fixed Deposit is one of the safest investment avenues, which can help you grow your savings, while offering stability and safety of principal amount. By investing in FD, you can take control of your investments, with greater flexibility, assured returns and high stability. Anyone can choose tenor between 12 months and 60 months, as per his financial needs.

In addition to attractive FD interest rates of up to 8.95% that offer greater returns, you can avail a suite of exciting features and benefits, such as choosing your tenor, or the frequency of your interest pay outs

Up to 8.95% Higher Return on Fixed Deposit. Higher Interest Rates for Senior Citizens – As high as 0.35% above the normal rate of Interest.

Minimum deposit of Rs. 25,000

High Stability and Credibility

CRISIL Rated : FAAA

ICRA Rated : MAAA

Assured Returns

&

Flexible Tenors

Online Account Management

When you invest in fixed deposits, you invest a principal amount at a fixed interest rate. You can then, gain interest on your deposits, which accrues and grows over time. Higher FD rates can enable you to gain a higher maturity amount, which is why you must choose lenders offering the highest interest rates in India. Bajaj Finance Fixed Deposit offers one of the highest interest rates in India, along with high safety ratings that ensure that your principal amount remain safe.

Log on to www.binduwasini.com

For further query please do call on to your

Relationship Manager.

For Assistance

Call on : +91-7875444433 or

Email to : binduwasini.advisor@gmail.com

With ICICI Lombard General Insurance Co. Ltd, Choosing a Insurance policy is not just for your tax purposes for every financial Year, but it should actually work for you when you are in need.

Health issues does not come or planned for they are sudden and we cannot plan this uncertainty. As do factors such as hospitalization cover and maternity cover or few others help us that moment and that don’t disturb or financial planning when we are medically insured

Health Insurance and Term Plan is a basic of FINANCIAL PLANNING. This covers our financial losses and help us to maintain our financial goals.

As a CERTIFIED FINANCIAL PLANNER we recommend these two product first before we go head with Financial Planning

Hospitalisation Cover : All expenses pertaining to in – patient hospitalisation such as room rent, intensive care unit charges, surgeon ’s and doctor’s fee, anaesthesia, blood, oxygen, operation theatre charges etc. incurred during hospitalisation for a minimum period of 24 consecutive hours are covered under the basic hospitalisation cover.

Day Care Surgeries / Treatments Coverage: All the medical expenses incurred while undergoing specified Day care Procedures /Treatment, as mentioned in the list, which requires less than 24 hours hospitalisation are covered

Pre and Post Hospitalisation Expenses: Medical expenses incurred immediately, 30 days before 60 days after Hospitalization will be covered by ICICI Lombard.

In Patient AYUSH Treatment : Expenses for Ayurveda, Yoga and Naturapthy, Unani, Siddha and Homeopathy (AYUSH) treatment only when it has been undergone in a government hospital or in any institute recognised by the government and / or accredited by Quality Council of India / National Accreditation Board on Health on Re - imbursement basis.

Reset Benefit: We will reset up to 100% of the base Sum Insured once in a policy year in case the Sum Insured including accrued additional Sum Insured (if any) is insufficient as a result of previous claims in that policy year.

Domestic Road Emergency Ambulance Cover: Reimbursement up to ` 1,500 per hospitalisation for reasonable expenses incurred on availing an ambulance service offered by a hospital /ambulance service provider in an emergency condition.

Additional Sum Insured: An Additional Sum Insured of 10% of Annual Sum Insured provided on each renewal for every claim free year up to a maximum of 50%. In case of a claim under the policy, the accumulated Additional Sum Insured will be reduced by 10% of the Annual Sum Insured in the following year.

Wellness Program: Our Wellness program intends to promote, incentivise and reward you for your healthy behaviour through various wellness services. All the activities as mentioned in the desired section help you earn wellness points which will be tracked by us.

Free Health Check up: The customer is entitled for a Free Health Check - up at designated centres. The coupons would be provided to each Insured for every policy year, subject to a maximum of 2 coupons per year for floater policies.

Hospital cash: A certain amount (as per the plan chosen) is paid for each and every completed day of hospitalization, such hospitalization is at least for a minimum 3 consecutive days subject to maximum 10 days in a policy year.

Convalescence Benefit: A benefit amount of ` 10,000 per insured once during the policy period will be paid in case of hospitalisation arising out of any injury or illness as covered under the policy, for a period of consecutive 10 days or more

Maternity Benefit: Reimbursement for medical expenses incurred for delivery, including a cesarean section, during hospitalisation or lawful medical termination of pregnancy during the policy period. The waiting period for maternity cover is 3 years. The cover shall be

limited to 2 deliveries / terminations during the period of insurance. Pre - natal and Post - natal expenses shall be covered under this benefit. This cover is applicable only for floater plan having Self and Spouse in the same policy for a continuous duration of 3 years. (Such waiting period shall reduce if the insured has been covered under a similar policy before opting for this policy, subject, however to the portability regulations).

New Born Baby Cover: The new born child can be covered under this policy during hospitalisation for a maximum period up to 91 days from the date of birth of the child. This cover will be provided only if maternity cover is opted.

Nursing at Home: An amount of ` 3,000 per day for a maximum of up to 15 days post hospitalisation for the medical services of a nurse at your residence.

Compassionate Visit (Air Travel For Family ): In the event of hospitalisation exceeding 5 days, the cost of economy class air ticket up to ` 20,000 incurred by the customer’s “immediate family member” while travelling to place of hospitalisation from the place of origin / residence and back will be reimbursed. "Immediate family member” would mean spouse, children and dependant parents.

Outpatient Treatment Cover: Reimbursement for the medical expenses incurred as an Outpatient (OPD) as per the plan chosen.

Wellness and Preventive Healthcare: All the expenses pertaining to routine health check - ups and for other wellness and fitness activities taken by you will be reimbursed up to the limit specified in the policy schedule.

Critical Illness Cover: The customer can opt for a Critical Illness Cover, covering specified Critical Illnesses /medical procedures such as Cancer of Specified Severity, Open Chest CABG, First Heart Attack - of Specified Severity, Kidney Failure Requiring Regular Dialysis, Major Organ / Bone Marrow Transplant, Stroke Resulting in Permanent Symptoms, Permanent Paralysis of Limbs, Open Heart Replacement or Repair of heart valves and End Stage Liver Disease. A benefit amount is paid up on the diagnosis of the chosen critical illness.

Donor Expenses: Reimbursement up to ` 50,000 for such medical expenses as incurred by the organ donor for undergoing any organ transplant surgery for your use.

Personal Accident Cover: The customer can also opt for a Personal Accident Cover where a fixed sum is paid upon the unfortunate event of Accidental Death or Permanent Total Disablement resulting from an accident. This cover can be availed only once during your lifetime. Once a claim becomes payable under this cover, no benefit will be provided under the same thereafter.

Medical Evacuation: Reimbursement of necessary and reasonable travel expenses, incurred as a result of evacuation to the nearest hospital under a medical emergency condition.

We will reset up to 100% of the base Sum Insured once in a policy year in case the Sum Insured including accrued additional Sum Insured (if any) is insufficient as a result of previous claims in that policy year, provided that:

For Reimbursement Claims: We shall make the payment of admissible claim (as per terms and conditions of Policy) OR communicate non admissibility of claim within 14 days after You submit complete set of documents and information in respect of the claims. In case We fail to make the payment of admissible claims or to communicate non admissibility of claim within the time period, We shall pay 1%interest over and above the claim within the time period, We shall pay 1% interest over and above the rate defined as per IRDAI (Protection of Policyholder's interest) Regulation 2002.

For Cashless Claims: If you notify pre - authorisation request for cashless facility through any of our empanelled network hospitals along with complete set of documents and information, we shall respond within 4 hours of the actual receipt of such pre authorisation request with:

Sub Limits: The customer can get the hospitalisation cover with a reduced premium by limiting the medical expenses pertaining to specified medical and surgical procedures as per below.

No Sub - Limits shall be applicable on any major medical illness and procedures and joint replacement surgery. Major medical illness and procedures for the purpose of this policy shall mean and include the following:

Mandatory Cover:

Hospitalisation+ In Patient AYUSH + Domestic Road Emergency Ambulance Cover + 2 Years PED + Reset Benefit + Wellness Program

Sum Insured:

5 Lakh ` 7 Lakh ` 10 Lakh ` 15 Lakh ` 20 Lakh ` 30 Lakh ` 50 Lakh

No-Sub Limit:

No Sub- limit available for and above ` 5 Lakh

Optional Add on Covers:

Hospital Daily Cash+ Convalescence Benefit + Critical illness + Donor Expense

During FY2018, ICICI Lombard settled 99.9 % health insurance claims and 90.8% motor insurance claims (own damage) within 30 days of claim filing.*

ICICI Lombard has been awarded as the Indian Insurance Award of ‘Claim Leader – General Insurance’ only validates why we remain your smartest choice.

ICRA (an Associate of Moody's Investors Service) has assigned iAAA rating indicating highest claims paying ability to ICICI Lombard General Insurance Company Limited.

The rating indicates a fundamentally strong position. Prospect of meeting policyholder obligations is the best. The rating takes into consideration ICICI Lombard's strong parentage, the high growth prospects for the general insurance business in the country, ICICI Lombard's strong capitalisation level, its prudent underwriting and reinsurance strategy, and its satisfactory underwriting performance.

We are associated with many authorized dealers in Pune for distributing forex cards to the travelling Indians (Tourist, Student, Work etc)

The rates are very competitive in terms of card fees. We deal in Multicurrency cards which are very useful for the overseas travellers.

We sale card for

We sale cards without any charges with the replacement cards for ICICI Bank Ltd.

We also help client for transferring the fund overseas through wire Transfer with competitive exchange rate through different bank channels.

ICICI Bank Travel Card

Introduction

The power-packed ICICI Bank Travel Card is the perfect travel companion for all your international trips. It is a smart, cost effective, convenient and secure alternative to carry foreign currency while travelling abroad. It offers instant loading and activation, enabling you to start using the card immediately after purchase for your international flight and hotel bookings

ICICI Bank Travel Card comes with an absolutely free Replacement Card that can be activated instantly in case of loss/ theft/ damage of the Primary Card. Besides protecting you from currency rate fluctuations, the card offers you great discounts at merchant outlets across the globe for your dining, shopping, stay and other expenses. It also provides many additional benefits including Comprehensive Travel Insurance, emergency travel assistance and zero lost card liability.

Features and Benefits of ICICI Bank Travel Card

Free Replacement Card in the kit

Your ICICI Bank Multicurrency Travel Card kit comes with a free Replacement Card along with the Primary Card. If you happen to lose/ damage the Primary Card, you can easily activate the Replacement Card.

Simply call up ICICI Bank Customer Care or the 24X7 International toll-free numbers to activate and transfer the balance on the Secondary Card. The ATM/ POS PIN is already available in the Travel Card Kit. In case you have forgotten or misplaced your PIN, it can be generated through Self-Care portal or by calling Customer Care.

Wallet to Wallet Transfer on Multicurrency Travel Card

Unsure of the amount to be loaded in each currency wallet while travelling to different countries? No need to worry anymore. Now transfer funds easily and instantly from one currency wallet to another by logging into Self Care Portal.

Duty Free shopping at Indian airports

While returning from an international trip, use the balance currency on your Travel Card at Duty Free stores to grab those last-minute souvenirs for your loved ones. This facility is enabled across all Indian airports.

ICICI Bank Multicurrency Travel Card is an ideal solution for frequent international travellers visiting multiple destinations. You can carry up to 15 currencies on a single card - USD, GBP, EUR, CAD, AUD, SGD, AED, CHF, JPY, SEK, ZAR, SAR, THB, NZD, HKD.

The card is enabled with a smart technology to automatically choose the currency wallet as per the local currency of transaction from the multiple available wallets on the card. Moreover, in case of insufficient balance in the wallet of transaction currency, the amount will be debited from the highest order wallet with sufficient balance.

Features and Benefits

Enjoy a hassle-free journey abroad with our Forex Card

The Forex Card is designed exclusively for customers who travel extensively across the globe. It is a unique product with multiple currencies loaded on the same card, thus eliminating the need to carry multiple cards for different destinations. The card, which is available on the VISA platform, also comes with exclusive dining privileges and the added benefit of Trip Assist - an emergency assistance in case of loss/theft of your card.

Contactless Forex Card

Powered by Visa’s payWave technology, the Forex Card will allow you to pay by simply ‘waving’ your card. With a secure, contactless CHIP technology, you will spend less time at the cash counter, thereby giving you the freedom to explore the destination to the fullest.

Image Forex Card

You can also design your own Forex Card with a personalised image of your choice or one from the unique designs available in the Image gallery. Capture the destinations you love, or relive memories from your favourite holidays, it’s all up to you!

A single card for multiple destinations

Load up to 16 currencies on a single card, and enjoy a hassle-free journey around the globe. Moreover, with just one card, you can use a single ATM PIN to access your account online or withdraw funds. Currencies available: USD( United States Dollars), EUR(Euro), GBP( Great Britian Pounds), SGD( Singapore Dollars), AUD(Australian Dollars), CAD(Canadian Dollars), JPY( Japanese Yen), CHF( Swiss Frank), SEK( Swedish Krona), THB (Thai Baht), AED( UAE Dirham), SAR (Saudi Riyal), HKD( Hongkong Dollars), NZD( Newzealand Dollars), DKK ( Danish Kroner) and ZAR ( South African Rand)..

Stay protected from currency fluctuations

With locked-in exchange rates, you won’t be paying cross-currency charges and will make your payments abroad at the rate you loaded/reloaded your card.

Validity of the Forex Card

The validity of the Forex Card is as mentioned on the card, during which you can reload it and use it for multiple trips.

Emergency assistance with TripAssist

In case of loss/theft of your Forex Card or wallet/baggage, you can get assistance with just one call! With TripAssist, you can:

24x7 access to your funds

Swipe your card at over 30 million Visa merchant outlets and 1,000 e-commerce websites, or withdraw funds from 1 million plus VISA ATMs.

Insurance coverage

The insurance that comes with your card covers:

Global Customer Assistance across the globe

Replace a lost card, or get emergency cash delivered while you are travelling overseas. Simply call Visa’s Global Customer Assistance Services to avail these services.

Notification alerts

Register your international mobile number and e-mail address to get instant alerts for every transaction.

Encash your funds once you return

Choose your option refill or refund or transfer to a dollar account. When you return from your trip, you can choose to

Submit a copy of the following documents along with the application form.

| Sr. | Document | At the time of Purchase | At the time of Reload |

| 1. | Passport Copy | Mandatory | Already Available - Not Required |

| 2. | Application Form | Mandatory |

|

| 3. | Visa | Mandatory | Same trip not required |

| 4. | Airline Ticket | Mandatory | Compulsory in case of next trip Same trip not required |

| 5. | PAN Card | Mandatory | Required if not provided earlier |

| 6. | Aadhaar Card | Mandatory | Required |

Features and Benefits

International Fund Transfer

Axis Bank offers International Fund Transfer to any bank account abroad. We have arrangements with major banks across the globe for Fund Transfers through the SWIFT mode, which ensures secure and safe remittance to any place of your choice.

Fund Transfer through Axis Bank Branch

Axis bank extensive branch network in India gives you the reach to most parts of the world. Just walk into any Axis Bank Branch and fill in the requisite documentation and request for your International Fund transfer permitted under the various purposes listed under Master Circular No. 06/2012-13 dt. 02-07-2012 released by RBI. Visit any nearest Axis Bank branch between 9:30 a.m. to 4 p.m.

Now use the easy to fill electronic application form at ease instead of physical Application Form A2, generate the Web reference number, take a print of PDF file and submit the digitally filled form along with underlying documents (KYCs). To use Digital Application Form A2 for outward remittance.

International Fund transfer through branch is available in 16 currencies - United States Dollars (USD), Great Britain Pounds (GBP), EURO (EUR), Australian Dollars (AUD), Canadian dollars (CAD), Hong Kong Dollars (HKD), Swiss Francs (CHF), Singapore Dollars (SGD), Saudi Riyal (SAR), UAE Dirham (AED), Japanese Yen (JPY), Swedish kroner (SEK), New Zealand Dollar (NZD), Danish Kroner (DKK), Thai Baht (THB) & South African Rand (ZAR)

Liberalised Remittance Scheme

The following purposes of remittance have been subsumed under the Liberalised Remittance Scheme for a limit of USD 250,000 per Financial Year.

Check scheme highlights

How much foreign exchange can one buy when traveling abroad on private visits to a country outside India?

For private visits abroad, other than to Nepal and Bhutan, any resident can obtain foreign exchange up to an aggregate amount of USD 2,50,000, from an Authorised Dealer or FFMC, in any one financial year, irrespective of the number of visits undertaken during the year. This limit has been subsumed under the Liberalised Remittance Scheme w.e.f. May 26, 2015. If an individual has already remitted any amount under the Liberalised Remittance Scheme in a financial year, then the applicable limit for travelling purpose for such individual would be reduced from USD 250,000 by the amount so remitted.

The resident individuals shall have to fill Form A2 and ‘Application cum declaration for purchase of foreign exchange under LRS of USD 250,000’ while availing foreign exchange for travelling purposes from AD banks and FFMCs.

No foreign exchange is available for visit to Nepal and/or Bhutan for any purpose. A resident Indian is allowed to take INR of denomination of Rs.100 or lesser denomination, to Nepal and Bhutan, without any limits. For denominations of Rs 500 and Rs1,000, the limit is Rs 25,000.

Further, all tour related expenses including cost of rail/road/water transportation charges outside India and remittances relating towards cost of Euro Rail; passes/tickets, etc. for Indian travellers, and overseas hotel/flight charges have been subsumed under the new enhanced limit of USD 250,000. The tour operator can collect this amount either in INR or in FCY.

How much foreign exchange can a person resident in India remit towards maintenance of close relatives abroad?

A person resident in India can remit up-to USD 250,000 per financial year towards maintenance of close relative (‘relative’ as defined in section 6 of the Companies Act, 1956) abroad. This limit has been subsumed under the Liberalised Remittance Scheme w.e.f. May 26, 2015. If an individual remit any amount under the Liberalised Remittance Scheme in a financial year, then the applicable limit for such individual would be reduced from USD 250,000 by the amount so remitted.

How much foreign currency can be carried in cash for travel abroad?

Travellers going to all countries other than (a) and (b) below are allowed to purchase foreign currency notes / coins only up to USD 3000 per visit. Balance amount can be carried in the form of travellers cheque or banker’s draft. Exceptions to this are (a) travellers proceeding to Iraq and Libya who can draw foreign exchange in the form of foreign currency notes and coins not exceeding USD 5000 or its equivalent per visit; (b) travellers proceeding to the Islamic Republic of Iran, Russian Federation and other Republics of Commonwealth of Independent States who can draw entire foreign exchange (up-to USD 250, 000) in the form of foreign currency notes or coins. For travellers proceeding for Haj/ Umrah pilgrimage, full amount of BTQ entitlement

How much foreign exchange is available to a person going abroad on emigration?

A person going abroad on emigration can draw foreign exchange from AD Category I bank and AD Category II up to the amount prescribed by the country of emigration or USD 250,000. This amount is only to meet the incidental expenses in the country of emigration. Further, this remittance is not for undertaking any capital account transactions such as overseas investment in government bonds; land; commercial enterprise; etc. No amount of foreign exchange can be remitted outside India to become eligible or for earning points or credits for immigration.

How much foreign exchange is available for a business trip?

For business trips to foreign countries, resident individuals/ individuals having proprietorship firms can avail of foreign exchange up to USD 2,50,000 in a financial year irrespective of the number of visits undertaken during the year. This limit has been subsumed under the Liberalised Remittance Scheme w.e.f. May 26, 2015.

Visits in connection with attending of an international conference, seminar, specialised training, apprentice training, etc., are treated as business visits. Release of foreign exchange exceeding USD 2,50,000 for business travel abroad, irrespective of the period of stay, by residents require prior permission from the Reserve Bank.

However, if an employee is being deputed by a company and the expenses are borne by the company, then such expenses shall be treated as residual current account transactions and may be permitted by the AD bank, without any limit, subject to verifying the bona-fides of the transaction.

Is there any category of visit which requires prior approval from the Reserve Bank or the Government of India?

Dance troupes, artistes, etc., who wish to undertake cultural tours abroad, should obtain prior approval from the Ministry of Human Resources Development (Department of Education and Culture), Government of India, New Delhi.

How many days in advance one can buy foreign exchange for travel abroad?

Permissible foreign exchange can be drawn 60 days in advance. In case it is not possible to use the foreign exchange within the period of 60 days, it should be immediately surrendered to an authorized person. However, residents are free to retain foreign exchange up to USD 2,000, in the form of foreign currency notes or TCs for future use or credit to their Resident Foreign Currency (Domestic) [RFC (Domestic)] Accounts.

Is there any time-frame for a traveller who has returned to India to surrender foreign exchange?

On return from a foreign trip, travellers are required to surrender unspent foreign exchange held in the form of currency notes and travellers’ cheques within 180 days of return. However, they are free to retain foreign exchange up to USD 2,000, in the form of foreign currency notes or TCs for future use or credit to their Resident Foreign Currency (Domestic) [RFC (Domestic)] Accounts.